Green Mountain: Over $300 Or Under $10? The Next Few Weeks Are Key

GMCR - Going to Over $300, or under $10?

Green Mountain Coffee Roasters (GMCR), a business that has emerged as the undisputed leader in the pre-packaged, single-brew coffee market, has not been kind to its long-term shareholders over the past 18 months, from a blowoff peak of $115.00/share, to a rock-bottom low of $17.00/share in a rapid 10-month wallop. I am going to make the case that we will either see a short-term period of consolidation and price decline that will present a good buying opportunity in a burgeoning long-term trend, or that GMCR has another major leg of decline that may take it down to the single digits; at that point, it will be one of the best buying opportunities around.

A Value Story, Yet?

GMCR has a lot of things that I like for a long-term buy; it has major price depreciation off of a hugely participated rally. It has demonstrated resilience and revenue increases while its share price was getting hammered. The company's vision has continued to expand into new markets and opportunities, while still maintaining a dominance over the K-Cup market by keeping its keen edge in quality manufacturing.

With GMCR still down over 60% off of its 2011 highs, is it cheap? Let's take a look:

(click to enlarge)

Its net book value has never been higher. GMCR has continued to generate positive cash flow and an increase in net value, even in the face of crushing 80%+ losses of share value. This is an impressive achievement, and speaks to the resilience of management to maintain a positive trajectory while investor pessimism fell off a cliff.

Compared to its previous history, it is just coming off of all time Price/Book lows of 1.5. At 2.8x price to book right now, it's certainly not dirt-cheap, but it is significantly lower than a great portion of the overall market (especially the NASDAQ), and far below its two previous overvalued extremes at 12x and 14x price/book.

Its price to earnings is at almost its lowest point ever, at a current 18.15, including forward P/E of 15.14.

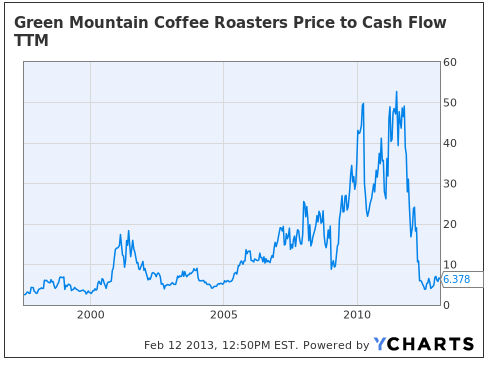

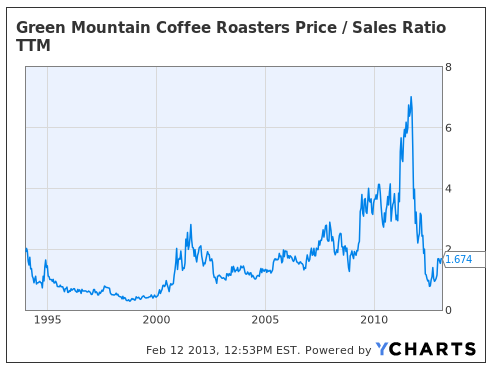

In terms of sales and cash flow, GMCR is still sitting at the bottom range of its historical multiples, presenting investors with a strong level of gross revenue and internal cash flow for every dollar invested.

(click to enlarge)

(click to enlarge)

There is certainly far deeper value potential if broad markets turn pessimistic, but GMCR will likely act more as a leading stock in this sort of a scenario, as a lot of pessimism is baked into its price action and we are just rebounding off of what is either a cyclical low, or a correction of its entire trend to date. There are far more overextended places an investor can place his money than in GMCR.

The Revenue Story

One of the major concerns for shareholders was the expiration of certain patents on their K-Cup design - not all of the patents, which has been a bit of a trick for competitors in terms of quality of the actual cups themselves.

This is because the original patents for the original K-Cup didn't turn out to be the most effective design. A more recent patent application (expiring in 2020) from Keurig, prior to GMCR's acquisition, had the following to say:

So, essentially, GMCR still has an artificial monopoly on "more flavor," as all of its competitors have to use an outdated design that just doesn't produce good enough tasting coffee for GMCR to sign off on. This will last until 2023, assuming they take no further steps to innovate and file any more patents, essentially keeping competitors two steps behind the development process the entire time.

As of a few months ago, when this patent business was just coming to a head, GMCR was actually adding new major coffee companies to its list of partnerships, despite loud calls for the opposite to happen upon patent expiration. Caribou signed a contract for 5 years in December 2011, Snapple signed up with GMCR in October of 2012. Folgers, Dunkin' Donuts, and Starbucks all have partnership agreements with GMCR to manufacture K-cups.

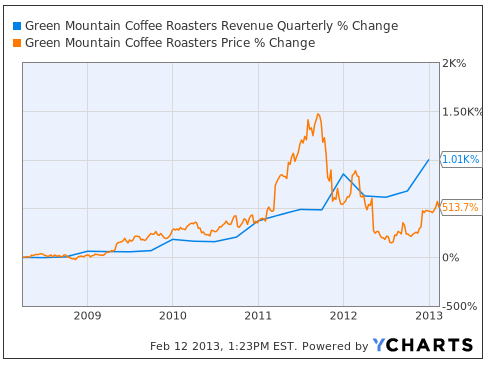

GMCR has seen impressive revenue growth over the past five years, and it currently sits at a place where its accumulated revenue growth is almost double its share price growth over the past 5 years. This is a welcome picture for would-be longs, demonstrating that pessimism versus reality is keeping share prices very conservative to other options.

(click to enlarge)

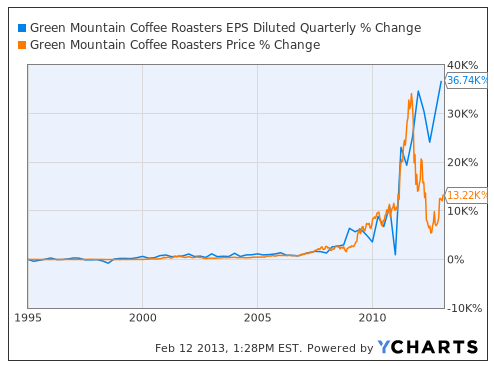

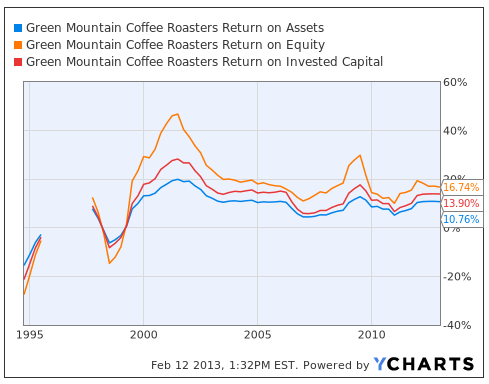

Not only that, but management has shown an effective hand at ensuring that net earnings growth continues, with EPS cumulative growth outstripping price growth by nearly 300% since the shares went public. That, and internal returns on equity, assets, and invested capital are all still at healthy levels.

(click to enlarge)

(click to enlarge)

The Future

The world loves coffee. Let's face it. Over 2.2 billion cups were consumed per day in 1999, and that number has continued climbing. Despite this, improvements in production have steadily increased annual worldwide yields, going back centuries.

(click to enlarge)

After the coffee price peak in early 2011 at about 320 cent/lb, very high on the historical range (thankfully without the irrational "peak" calls that liquidity-induced blow-offs seem to inflame, as with oil). It has since cooled off to the tune of 50%, which will only make coffee that much more affordable and widely available to consumers - GMCR has a better set of updated negotiations with its bean suppliers, and even though the margin impact will be small, when you're selling billions of K-cups for year, even a single penny adds up, and fast.

(click to enlarge)

Due to its wide-spread partnerships with heavily capitalized existing coffee sellers, its two-steps-ahead patent structure, and the hugely positive reception to the K-cup revolution by the general public, all in the face of a decimated share price, I am very positive about GMCR's future.

Two Current Options - Short-Sell for the Brave. Wait, for the Patient Long.

I am very optimistic about GMCR's long-term prospects for the future. Investors have been too quick to move on to other bull-traps like Netflix, Amazon, Google, and others, and have left GMCR as a cheap prospect for smart investors.

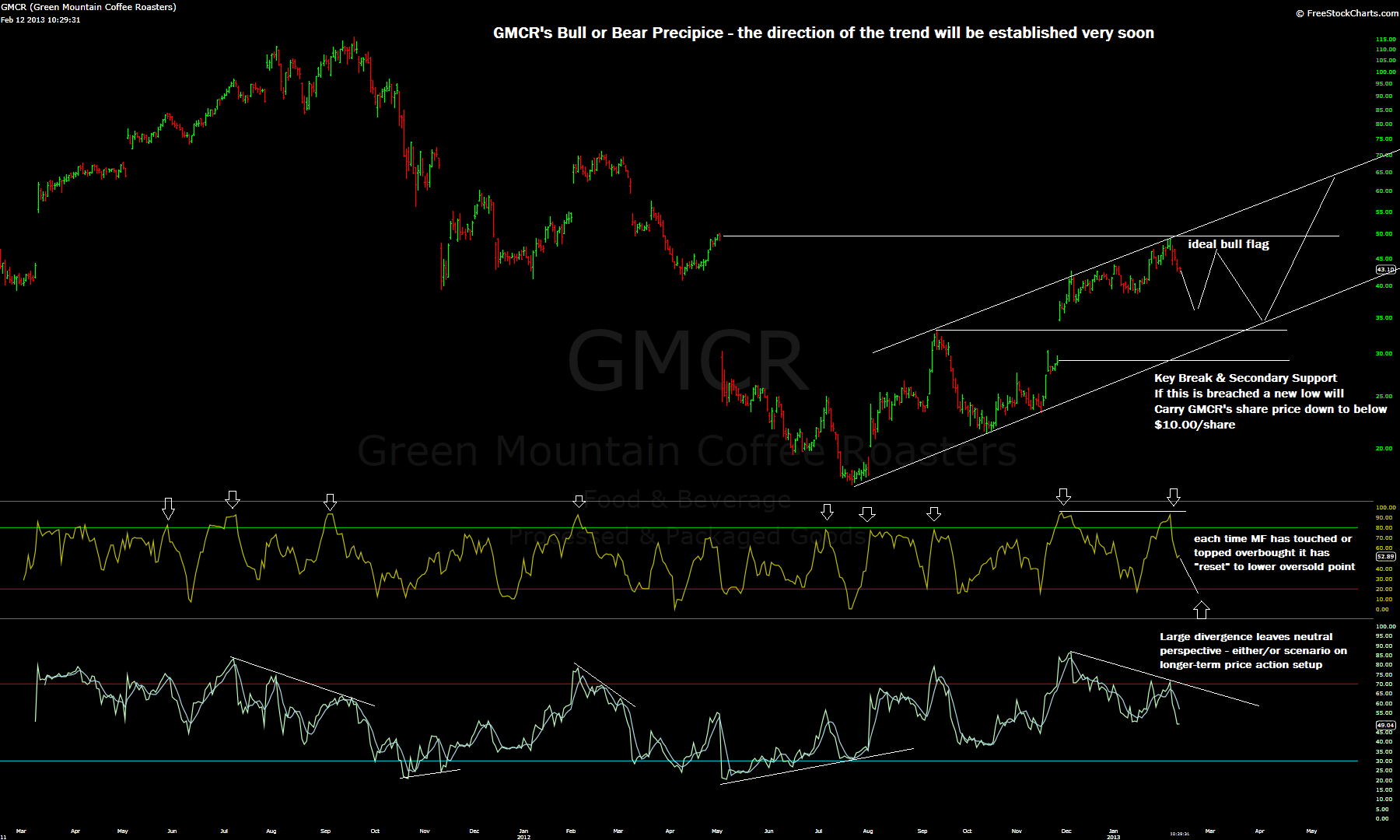

That being said, the optimistic run up to earnings has carried the stock to a short-term overbought level that has started to unwind. Furthermore, it is at a critical juncture - the next several weeks or so should determine if this entire rally from last year's lows is laying the foundation for a new cyclical bull market in GMCR, or if it is simply capping off a motive correction from last year, and will put in another leg down to correct the entire 1990's uptrend.

I am leaning more towards the former, but the price action will speak for itself, and when it does, it should be definitive.

Here's the grand picture for GMCR. There are two major options as per the tendencies of long-term investor buying and selling activity (optimism versus pessimism).

(click to enlarge)

If we are going to expect more selling, it should commence immediately and carry the price action down into the territory of its first up-leg, breaching the $33.00/share mark and strongly following through. This will indicate that the larger downtrend is not complete, and signal a carrythrough that will erase all of the gains of the prior 7 months or so. If this is the case, I have set the long term entry point for $9.00/share, with optimal entry being at the $4.80 mark or so.

If the share price holds above the $33.00 mark and begins another leg up after this internal momentum reset is complete, that would indicate a brand new impulsive, multi-year leg up is underway, and that will likely take GMCR all the way to the top of its historical price channel, meaning over $400/share.

I have labeled the key points on the following chart:

(click to enlarge)

Could GMCR's Fundamental History Justify A Move Over $300?

Consensus topline revenue and net earnings, annually, through 2013-2014 are $2.80/share on $4.5 Billion in revenue for 2013, and $3.15/share on $5.1 billion for 2014. If we look at historical extreme valuations on the charts above in terms of price/sale, and price/earnings, we come up with a pretty lofty price target at elevated optimism:

At its real historical extreme of 7.1 price/sales, were GMCR to have $5.1 billion in 2014, it would be within reason to see a $36.21 billion market cap. This would equate to a per share price of $263.11/share. Using its historical price-to-earnings peak of 120 during its 2011 peak, this would put GMCR stock at $363.60 at earnings of $3.15/share.

So it would be within historical norms, albeit the remnant edges of those norms, to see another huge leg up in GMCR's share price if optimism begins to take off again and the numbers follow along the consensus and guidance lines.

The Action Plan - What to Do, Buy Or Sell?

Short-term, GMCR is a short-sell to alleviate the overbought condition. Historically, the daily money flow metric has rolled right down to the oversold area upon a trend change, and it is only about halfway toward that mark. RSI has also diverged very hard, on a daily basis, and ideally would see a reset down into the low 40s or below. If GMCR is simply taking a breather here, a strong price target would be previous short-term support on the still-young channel up from last year's lows, at $35.00/share. Because the last correction was sharp and swift, expect more of a sideways-down action if this is indeed simply a breather and not a major peak.

A short sell at these levels, $44.00/share, and a move to the far side of the channel would generate a yield of $9.00/share, or 20% gains. I recommend setting a stop at the prior peak of $49.00 if you short-sell, which creates a 2:1 risk/reward for the short term, and a clear point where a break would determine the larger trend was up - at that point, I recommend a fully leveraged long position as GMCR is headed on to far higher highs.

If the price moves swiftly down and breaches below $33.00/share, this indicates that a larger downtrend has started, and short-sellers can target a longer-term position to below $10/share.

Conclusions

GMCR has demonstrated its resilience in the face of a huge downturn in share prices and a big uptick in investor pessimism. This alone is an impressive achievement. It is already sitting at conservative valuations relative to its prior performance, still owns the most pertinent patents to the modern K-cup game, and has strategic partnerships with many major coffee brands. Sales should continue to be strong and cash flow very positive.

GMCR is either a long-term buy right now, or it is going to be within a fairly short time. It is currently consolidating and correcting a very overbought condition, and the next few weeks will reveal if it is beginning an entirely new bull market leg that will eventually carry it on to new, all-time highs over $300/share, or if it is ready to continue its slide and make a new low off of its 2011 highs. I recommend a short term short-sale with a target of $35.00/share, a stop placed at $44.00/share which will also act as a signal for a long term, larger long position. In the event of a break off $33.00, I have a short-sell cover target of $9.00/share and a long-term buy in place at that point.

Green Mountain Coffee Roasters (GMCR), a business that has emerged as the undisputed leader in the pre-packaged, single-brew coffee market, has not been kind to its long-term shareholders over the past 18 months, from a blowoff peak of $115.00/share, to a rock-bottom low of $17.00/share in a rapid 10-month wallop. I am going to make the case that we will either see a short-term period of consolidation and price decline that will present a good buying opportunity in a burgeoning long-term trend, or that GMCR has another major leg of decline that may take it down to the single digits; at that point, it will be one of the best buying opportunities around.

A Value Story, Yet?

GMCR has a lot of things that I like for a long-term buy; it has major price depreciation off of a hugely participated rally. It has demonstrated resilience and revenue increases while its share price was getting hammered. The company's vision has continued to expand into new markets and opportunities, while still maintaining a dominance over the K-Cup market by keeping its keen edge in quality manufacturing.

With GMCR still down over 60% off of its 2011 highs, is it cheap? Let's take a look:

(click to enlarge)

Its net book value has never been higher. GMCR has continued to generate positive cash flow and an increase in net value, even in the face of crushing 80%+ losses of share value. This is an impressive achievement, and speaks to the resilience of management to maintain a positive trajectory while investor pessimism fell off a cliff.

Compared to its previous history, it is just coming off of all time Price/Book lows of 1.5. At 2.8x price to book right now, it's certainly not dirt-cheap, but it is significantly lower than a great portion of the overall market (especially the NASDAQ), and far below its two previous overvalued extremes at 12x and 14x price/book.

Its price to earnings is at almost its lowest point ever, at a current 18.15, including forward P/E of 15.14.

In terms of sales and cash flow, GMCR is still sitting at the bottom range of its historical multiples, presenting investors with a strong level of gross revenue and internal cash flow for every dollar invested.

(click to enlarge)

(click to enlarge)

There is certainly far deeper value potential if broad markets turn pessimistic, but GMCR will likely act more as a leading stock in this sort of a scenario, as a lot of pessimism is baked into its price action and we are just rebounding off of what is either a cyclical low, or a correction of its entire trend to date. There are far more overextended places an investor can place his money than in GMCR.

The Revenue Story

One of the major concerns for shareholders was the expiration of certain patents on their K-Cup design - not all of the patents, which has been a bit of a trick for competitors in terms of quality of the actual cups themselves.

This is because the original patents for the original K-Cup didn't turn out to be the most effective design. A more recent patent application (expiring in 2020) from Keurig, prior to GMCR's acquisition, had the following to say:

...the configuration of the filter element encourages rapid liquid penetration to and through the lower end, resulting in less than optimum saturation of the beverage medium at upper regions of the filter element adjacent to the container wall. The combined effect of limited storage capacity and less than optimum saturation is a lowering of the total dissolved solids ("TDS") in the brewed beverage, which translated into reduced flavor.This later attempt was then, too, abandoned, for a further-modified design that finally managed to get the K-Cup up to a level of flavor that Keurig & GMCR found acceptable. This is the design that they currently use, and the application is still pending in the US, has actually be meta-filed through an international organization that stretches across 140 countries. Canada has already approved the patent for the latest design, which can be found here, and doesn't actually expire until 2023.

So, essentially, GMCR still has an artificial monopoly on "more flavor," as all of its competitors have to use an outdated design that just doesn't produce good enough tasting coffee for GMCR to sign off on. This will last until 2023, assuming they take no further steps to innovate and file any more patents, essentially keeping competitors two steps behind the development process the entire time.

As of a few months ago, when this patent business was just coming to a head, GMCR was actually adding new major coffee companies to its list of partnerships, despite loud calls for the opposite to happen upon patent expiration. Caribou signed a contract for 5 years in December 2011, Snapple signed up with GMCR in October of 2012. Folgers, Dunkin' Donuts, and Starbucks all have partnership agreements with GMCR to manufacture K-cups.

GMCR has seen impressive revenue growth over the past five years, and it currently sits at a place where its accumulated revenue growth is almost double its share price growth over the past 5 years. This is a welcome picture for would-be longs, demonstrating that pessimism versus reality is keeping share prices very conservative to other options.

(click to enlarge)

Not only that, but management has shown an effective hand at ensuring that net earnings growth continues, with EPS cumulative growth outstripping price growth by nearly 300% since the shares went public. That, and internal returns on equity, assets, and invested capital are all still at healthy levels.

(click to enlarge)

(click to enlarge)

The Future

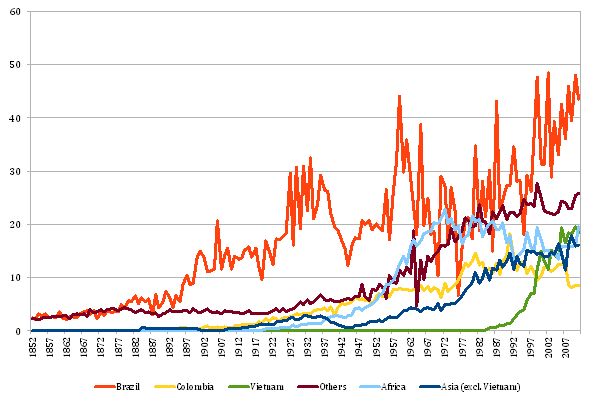

The world loves coffee. Let's face it. Over 2.2 billion cups were consumed per day in 1999, and that number has continued climbing. Despite this, improvements in production have steadily increased annual worldwide yields, going back centuries.

(click to enlarge)

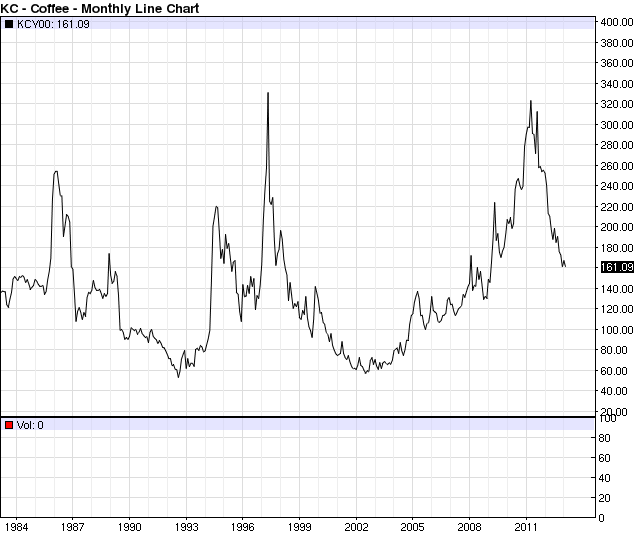

After the coffee price peak in early 2011 at about 320 cent/lb, very high on the historical range (thankfully without the irrational "peak" calls that liquidity-induced blow-offs seem to inflame, as with oil). It has since cooled off to the tune of 50%, which will only make coffee that much more affordable and widely available to consumers - GMCR has a better set of updated negotiations with its bean suppliers, and even though the margin impact will be small, when you're selling billions of K-cups for year, even a single penny adds up, and fast.

(click to enlarge)

Due to its wide-spread partnerships with heavily capitalized existing coffee sellers, its two-steps-ahead patent structure, and the hugely positive reception to the K-cup revolution by the general public, all in the face of a decimated share price, I am very positive about GMCR's future.

Two Current Options - Short-Sell for the Brave. Wait, for the Patient Long.

I am very optimistic about GMCR's long-term prospects for the future. Investors have been too quick to move on to other bull-traps like Netflix, Amazon, Google, and others, and have left GMCR as a cheap prospect for smart investors.

That being said, the optimistic run up to earnings has carried the stock to a short-term overbought level that has started to unwind. Furthermore, it is at a critical juncture - the next several weeks or so should determine if this entire rally from last year's lows is laying the foundation for a new cyclical bull market in GMCR, or if it is simply capping off a motive correction from last year, and will put in another leg down to correct the entire 1990's uptrend.

I am leaning more towards the former, but the price action will speak for itself, and when it does, it should be definitive.

Here's the grand picture for GMCR. There are two major options as per the tendencies of long-term investor buying and selling activity (optimism versus pessimism).

(click to enlarge)

If we are going to expect more selling, it should commence immediately and carry the price action down into the territory of its first up-leg, breaching the $33.00/share mark and strongly following through. This will indicate that the larger downtrend is not complete, and signal a carrythrough that will erase all of the gains of the prior 7 months or so. If this is the case, I have set the long term entry point for $9.00/share, with optimal entry being at the $4.80 mark or so.

If the share price holds above the $33.00 mark and begins another leg up after this internal momentum reset is complete, that would indicate a brand new impulsive, multi-year leg up is underway, and that will likely take GMCR all the way to the top of its historical price channel, meaning over $400/share.

I have labeled the key points on the following chart:

(click to enlarge)

Could GMCR's Fundamental History Justify A Move Over $300?

Consensus topline revenue and net earnings, annually, through 2013-2014 are $2.80/share on $4.5 Billion in revenue for 2013, and $3.15/share on $5.1 billion for 2014. If we look at historical extreme valuations on the charts above in terms of price/sale, and price/earnings, we come up with a pretty lofty price target at elevated optimism:

At its real historical extreme of 7.1 price/sales, were GMCR to have $5.1 billion in 2014, it would be within reason to see a $36.21 billion market cap. This would equate to a per share price of $263.11/share. Using its historical price-to-earnings peak of 120 during its 2011 peak, this would put GMCR stock at $363.60 at earnings of $3.15/share.

So it would be within historical norms, albeit the remnant edges of those norms, to see another huge leg up in GMCR's share price if optimism begins to take off again and the numbers follow along the consensus and guidance lines.

The Action Plan - What to Do, Buy Or Sell?

Short-term, GMCR is a short-sell to alleviate the overbought condition. Historically, the daily money flow metric has rolled right down to the oversold area upon a trend change, and it is only about halfway toward that mark. RSI has also diverged very hard, on a daily basis, and ideally would see a reset down into the low 40s or below. If GMCR is simply taking a breather here, a strong price target would be previous short-term support on the still-young channel up from last year's lows, at $35.00/share. Because the last correction was sharp and swift, expect more of a sideways-down action if this is indeed simply a breather and not a major peak.

A short sell at these levels, $44.00/share, and a move to the far side of the channel would generate a yield of $9.00/share, or 20% gains. I recommend setting a stop at the prior peak of $49.00 if you short-sell, which creates a 2:1 risk/reward for the short term, and a clear point where a break would determine the larger trend was up - at that point, I recommend a fully leveraged long position as GMCR is headed on to far higher highs.

If the price moves swiftly down and breaches below $33.00/share, this indicates that a larger downtrend has started, and short-sellers can target a longer-term position to below $10/share.

Conclusions

GMCR has demonstrated its resilience in the face of a huge downturn in share prices and a big uptick in investor pessimism. This alone is an impressive achievement. It is already sitting at conservative valuations relative to its prior performance, still owns the most pertinent patents to the modern K-cup game, and has strategic partnerships with many major coffee brands. Sales should continue to be strong and cash flow very positive.

GMCR is either a long-term buy right now, or it is going to be within a fairly short time. It is currently consolidating and correcting a very overbought condition, and the next few weeks will reveal if it is beginning an entirely new bull market leg that will eventually carry it on to new, all-time highs over $300/share, or if it is ready to continue its slide and make a new low off of its 2011 highs. I recommend a short term short-sale with a target of $35.00/share, a stop placed at $44.00/share which will also act as a signal for a long term, larger long position. In the event of a break off $33.00, I have a short-sell cover target of $9.00/share and a long-term buy in place at that point.

No comments:

Post a Comment