Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Describing Warren Buffett as one of the most admired

investors in the world is like describing California as one of our most

populous states. As a result of the pedestal on which Buffett stands,

many seek to apply his methods to their own investing activity and some

have even developed quantitative models purporting to do so, including

the one I created for use on Portfolio123.com.The Challenge

Generally, it's good to use such approaches, not because they really replicate what Buffett does - see below - but because the factors they use are sound and would be so even if advocated by John Doe. Still, there's often an element of frustration for users because as one scans the lists, it seldom takes long to find a stock at which one can point and shout: "No way Buffett would buy this, and I can prove it; look here on page such and such in this book about Buffett!"

There's much to be said for such skeptics. As far as I or anyone can tell, Buffett does not use computerized screening or ranking tools. And although much has been said over the years by Buffett in the Berkshire Hathaway (BRK.B) annual shareholder letters and by others in books, there is no reason to believe that each factor Buffett considers is treated as being equally important to each decision on each stock. We know for example that Buffett considers returns on equity, margins, owner earnings (a variation on cash flow net of capital spending), and valuation among other things. But we don't know that he has a specific, unalterable, numerical threshold in mind for each decision he makes or even that all such metrics must be part of all his decisions. In other words, if Buffett is looking at valuation and return on equity, it's possible (very possible since his greatest success predate computerized tools) he may relax his return-on-equity expectations if he's sufficiently impressed with a stock's value and do the opposite on other occasions and exhibit similar flexibility with all the metrics in his repertoire.

In addition, there are other considerations deemed vital by Buffett that are not amenable to any sort of quantitative modeling, such as the extent to which he is confident in a company's top executives or the "inevitability" of its business model. Although we Buffett followers may hate to admit it, there is much we cannot replicate - that which is based on Buffett's own unique genius. You can't screen for that!

The Solution

I decided, therefore, to start from scratch with a new approach. Screening and ranking are at the core of what I do, so I'm going to stick with that. But rather than attempt to pull a bunch of screening rules and ranking factors from the Buffett oeuvre, I'm using my own rules and factors to create a model that is inspired by three important and in my view quantifiable concepts that are driven home by studying Buffett: fair valuation, solid company fundamentals, and reasonable consistency.

The most challenging aspect of following Buffett is his quest for inevitability; companies that are doing well now are likely to be doing well next year, are likely to be doing well ten years from now, are likely to be doing well twenty years from now, etc. Rhetoric along these lines is irresistible, but implementation is a challenge since we humans are not nearly as good at forecasting the future as we like to presume. Warren Buffett likewise is not clairvoyant. But he does give it a try.

Indeed, Buffett's well-known aversion to technology stems directly from his quest for "inevitables." It's not, as many assume, a matter of his not understanding the business. While neither he nor most other investors would, for example, be able to discourse on semiconductors the way an engineer would, that's not necessarily the roadblock. We know that as of the last Berkshire annual report, ConocoPhillips (COP) was in the company's portfolio. Do you think Buffett can discourse on the geological properties of different oilpatch properties, or of drilling techniques, etc.? Berkshire owned Kraft Foods (KRFT), but I don't imagine Buffett knows much more, if any more, about large-scale food preparation, packaging, shipping etc. than any of us (at least any of us who don't work for companies like Kraft).

The comprehension he seeks, and which technology hasn't been offering, deals with the general nature of the business: short product cycles, harder-to-anticipate and frequently-emerging competitive threats, high development costs, etc. It's one thing to look at COP or KRFT and even without an insider's deep knowledge of the detailed ins and outs of the business assume those companies will still be viable ten years from now. It's a very different matter when it comes to Intel (INTC) or even Apple (AAPL). This is why Buffett has been leery of technology. My model follows him in this regard and excludes tech.

Beyond that, the presence or absence of inevitability is a judgment call. The good news for Buffett is that he, while not perfect, has been pretty darn good over a prolonged period of time. The bad news is that the workings of his mind in this area cannot be reduced to a quantitative model. So I don't pretend to be able to identify inevitability. Instead, my approach searches for a long track record of consistency - not perfection (few companies, including Buffett holdings, offer that) but general long-established consistency.

So in sum, this isn't Buffett per se. The only way to really get that is to own Berkshire stock. Instead this is my model based not on each and every idea associated with Buffett but on the ones that strike me as most significant and amenable to modeling.

Can It Work?

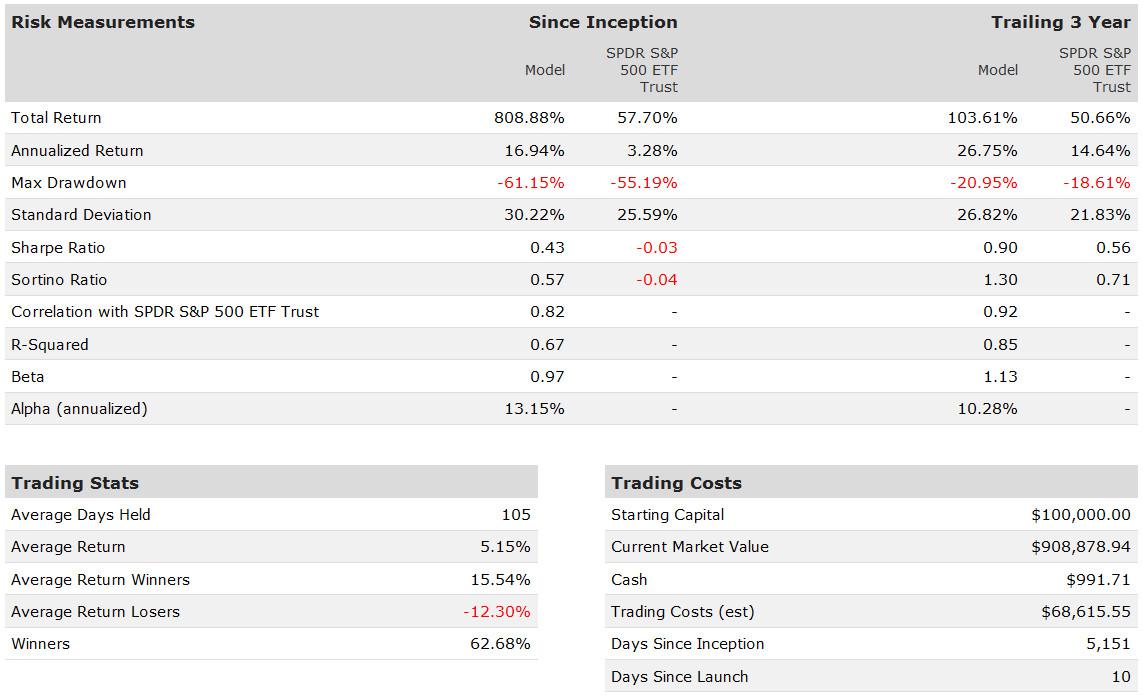

Figures 1, 2 and 3 show backtested performance data for the Buffett model I create for Portfolio123's new selection of Ready-2-Go models. It's important to recognize that this is a point-in-time test, meaning there is no survivorship bias (companies in the S&P 500 benchmark and the Buffett portfolio are those that were in existence at relevant times in the past, even though they may no longer exist today) and no look-ahead bias (the model uses data as of the date it was available to the investment community; for example, year-end 2011 data was not used on 1/1/12 but later, when it was reported by the companies and added to the Compustat database.

Figure 1

(click to enlarge)

Figure 2

(click to enlarge)

Figure 3

(click to enlarge)

Trading cost is necessarily a rough estimate since we cannot know in advance any user's brokerage arrangement or starting capital. Our figures are based on an assumption of 0.20% price slippage per trade. That said, when I trade using models like this, I use FolioInvesting.com, where a willingness to trade in one of the firm's twice-daily trading windows (at 11 AM or 2 PM, ET) allows an investor to bring transaction costs as close to zero as they can reasonably be expected to go.

Out-of-sample performance data is necessarily very limited since the Ready-2-go section debuted just this month. But here's what we have so far.

Figure 4

(click to enlarge)

The first of the model's four-week rebalancings to occur in the "live" period occurred on 2/11/13. Of the 20 stocks in the portfolio, six were sold. Here are the six new replacement positions:

Green Mountain Coffee Roasters (GMCR)

Just my luck, the first company up in my alphabetical listing has to be this one, which at times might have re-named Controversy, Inc. But for what it's worth, Buffett, as homespun as people like to think he is, has had his share of corporate excitement, most notably his ill-starred and sizable stake in Salomon Brothers, which was later so badly tainted by scandal Buffett actually left Omaha to take up residence in New York City to serve temporarily as CEO and set the firm straight. There was also NetJets, internal issues with his one-time and now former heir apparent, not to mention some of his speculations in silver and derivatives which, before he speculated in them, he referred to financial weapons of mass destruction (the latter weren't necessarily bad ideas, but they clash sharply with Buffett's Norman Rockwell image). And besides, as it turns out, GMCR didn't actually do anything wrong.

By now, I think we all know what GMCR does but for those who may not, this is the company behind those Keurig single-serve coffee brewers and the K-cups (single-serve coffee-filled packets) they use. I fell in love with these gizmos more than a decade ago when I first saw them in an office in which I worked and was impressed by how easy the coffee-making process was and by the incredible variety (I had a particular passion for German Chocolate Cake flavored and Blueberry coffees). At that time, GMCR only produced coffee, and K-cups were an important part of its business. But when it acquired Keurig, the outfit that makes the brewing machines, I jumped into the stock and spent several years enjoying the ride. Eventually, I bailed out fearing valuation. (Actually GMCR appeared substantially overvalued every single day I owned the stock but I assumed, correctly it turned out, that the company would grow into its valuation metrics, but eventually I got financial vertigo and cashed in.)

Interestingly looking at it now, valuation is - finally - not a problem. The trailing 12 month P/E is a bit below 20, versus nearly 50 in 2011. The stock presently sells for 16 times estimated current-year EPS and 14 times estimated EPS for next year. Price/sales, at 1.71, isn't dirt cheap, but it's better than the 2011 3.74 average. And from 2011 to the present, price to free cash flow dropped from 29.41 to about 12 while price/book fell from a ridiculous 5.18 to a still-generous but not as insane 3. With an 18.33 percent Wall street consensus long-term EPS growth projection, the PEG ratio comes in at 0.88.

The key is whether the 18.33 percent growth-rate projection makes sense.

We have to expect deceleration from what GMCR did in the past. With GMCR having grown so much (annual sales are now around $4 billion, versus $162 million in 2005), deceleration is to be expected as a natural consequence of larger size. The patent the company held preventing others from making K-cups expired in 2012. And Starbucks (SBUX), presently a partner with GMCR through Starbucks-branded K-cups, has also become a rival through the introduction of its own single-serve brewer (though you'd never know it from the way demo models are shoved to inconspicuous locations at some of the Starbucks shops near where I live). But consider that GMCR is likely to decelerate from historical rates of sales growth that were often in the 40% range and rates of EPS growth that were quite a bit higher. A future 18.33% EPS growth rate would already incorporate a heck of a lot of slowdown.

That said, I don't think the GMCR story is anywhere near being over. Single-serve coffee is still a growing category (I don't think Starbucks would have jumped in if that was not the case). There's plenty of room for distribution to grow; supermarkets and drugstores are just now dipping their feet in the water. As to competition, the Starbucks machine is really a different, higher-end category that includes full brewing including milk and sweetener and other brew types (latte, etc.) and GMCR has its own upper end machine to fight SBUX in that category. And with the K-cup patent having expired, it's comforting to see that the market isn't being flooded with competitive offerings. Apparently, as GMCR maintains, there's something to be said for know-how and scale. But still, GMCR is being inspired by patent expiration to get serious about cost efficiency and the marketing of its proprietary coffee brands.

There are those who say a Buffettologist should require an economic moat. Hogwash! Regardless of what Buffett has said that inspired this nonsense, he's owned plenty of companies that don't have moats. In fact, few companies do. Remember when everyone wanted to break up Microsoft (MSFT) to combat that firm's stranglehold on the world! (Take time out for a laughter break if you need one.) The fact is that businesses must compete, all businesses. Buffett invests in companies that compete. So, too, does everyone else. And with the single-serve brewing market having a lot of growth ahead of it and with the stock tolerably valued, I'm comfortable with this selection, even though it will undoubtedly attract rhetoric from haters from time to time (there are a lot of shorts who need to rant loudly whenever they can, in response to future guidance shifts, etc., lest they be squeezed into oblivion).

Moog Inc. (MOG.A)

Here's one of many situations where the boundary between tech and non-tech gets fuzzy. The company makes motion-control products, which can get quite technological. But it's been around for a long time and customers, aircraft manufacturers, missile launch manufacturers, marine products manufacturers, medical products manufacturers, etc. don't retrofit equipment for new motion control gizmos as quickly as teens and twenty-somethings change smart phones. MOG.A has to stay fresh, of course, but its R&D is manageable, usually in the range of 4%-6% of sales. Capital spending can ramp up at times, as is the case for all manufacturers. But past projects, coupled with rising business performance, presently make this item quite tolerable at about half of cash from operations. Ultimately, though, MOG.A has demonstrated considerable consistency to date, enough so certainly to fit our theme, not so much by chasing fleeting tastes and protocols but by being effective at serving basic markets.

Aerospace is the largest end market served by the company (23% of sales for the military and 16% for commercial aircraft) with Space and Defense accounting for another 14%. The rest consists of Industrial (26%), Components (15%), and Medical Devices (6%). About 45% of the revenue base is international.

U.S. military sales may grow more slowly (many in Washington hope that will be the case), but military sales may grow more with other countries. Notwithstanding the battery mess with the 787 Dreamliner, we need lots and lots of new commercial planes so that area could be strong for a long time. Medical Devices seems interesting as a way to add some growth to the industrial area.

The biggest potential benefit to MOG.A is, simply, better global activity. That may require some patience. But with forward P/Es of 12.6 (based on the current-year EPS estimate) and 11.3 (based on next year's EPS estimate), we ought to be able to live with that.

Nu Skin Enterprises (NUS)

And I'll bet you thought you were done with controversy after you finished reading the section on Green Mountain: Nah, not by a long shot. OK. Let's try multi-level marketing!

Whoa there. Stop climbing out of the window. Take a deep breath. I'm not talking about Herbalife (HLF). The company going into the portfolio is Nu Skin.

Actually, I'm not sure how comforting that is. NUS, which deals with skin care products and nutritional supplements and is launching a weight-loss product, competes with HLF and both distribute via multi-level marketing, wherein the producing company sells to independent distributors who consume products themselves and, hopefully, sell a heck of a lot more product to others and make money through sales commissions and recruitment of other sales people. Oh darn, that probably does not make you feel better. I get it. Let's continue.

I have to confess straight up that I'm not going to be able to establish here whether HLF is, as has been alleged, a pyramid scheme and will leave that to the hedge-fund managers waging vigorous rhetorical battles and to regulators who are looking at HLF more closely (and presumably - hopefully - much more dispassionately). Nor can I tell you whether that is or is not the case for NUS.

But here are some things I can tell you. Multi-level marketing is a legitimate business; we cannot assume all who engage in it are doing anything wrong. Moreover, there are no allegations out there regarding NUS.

Going further, I compared sales and distributor trends for NUS and HLF and found some interesting differences. For starters, NUS's distributors seem substantially more effective than those of HLF and have been widening their lead over time. In terms of sales per distributor (regular distributors plus executive distributors or sales leaders), NUS's number was 83% greater than that of HLF in 2011, 74% greater in 2010, 79% greater in 2009, 61% greater in 2008, 49% greater in 2007 and 43% greater in 2006.

Here's a particularly interesting comparison between basic distributors and higher level distributors (those who've climbed in the hierarchy through superior sales and more likely recruitment of others to work as distributors under them in their networks; the terminology differs between HLF and NUS, but essentially, we're dealing here with sales leaders, executive distributors, supervisors, etc.). At NUS, higher-level distributors as a percent of the total has been in the vicinity of 4% and growing slowly: the numbers for each year from 2006 through 2011 are 3.8%, 3.8%, 3.9%, 4.1%, 4.3% and 4.7%. It's a very different story at HLF, where higher-level distributors are a much larger, but diminishing, percent of the total. From 2006 to 2011, the percentages were: 21.4%, 21.8%, 21.0%, 19.4%, 18.7%, and 16.9%.

This certainly does not prove that NUS is a good guy and HLF is a bad guy. But it does seem reasonable to infer that selling product has been a bigger priority for many of the typical NUS distributors than has been the case for his or her HLF counterparts; there does seem to be at least some indication that a lot more of the latter devote more effort into or wind up achieving more success in building networks than selling products. Does that make HLF a pyramid scheme? Again, the answer is "no." It may simply mean HLF isn't as good at network marketing as NUS. More importantly for our purposes, it supports the notion that the consistent business performance seen for NUS in the past is based on what we want it to be based on, selling product.

Here's one more interesting comparison between NUS and HLF. For each company, I compare annual percent change in sales with annual percent change in the total number of distributors.

Here are the numbers for HLF: 14% growth in both in 2007; 10% growth in sales and 11% growth in distributors in 2008; a 1% decline in sales and a 3% gain in distributors in 2009; an 18% gain in sales and a 4% gain in distributors in 2010; and 26% growth for in each in 2011.

Here are the numbers for NUS: 3.8% growth in sales and a 1% decline in distributors in 2007; 7.8% growth in sales and 1% growth in distributors in 2008; a 6.7% gain in sales and a negligible change in distributors in 2009, a 15.5% gain in sales and a 5% gain in distributors in 2010; and 13.4% growth in sales and a 7% gain in distributors in 2011.

It appears, therefore, that except for HLF's unusually strong year in 2010, NUS has been noticeably better in what I suppose we might refer to as same-distributor sales growth.

I really didn't mean to deal be so much with HLF. But given the rhetorical fireworks surrounding that company, we pretty much have to address it if we are to consider rival and peer NUS. Meanwhile, the latter does seem to be legitimately selling product (and for the record, a lot of this occurs outside the U.S., particularly in Asia), and the stock is modestly valued, trading at 10.5 times the estimate of current-year EPS and 9.3 times the estimate for next year. Even though NUS is probably not the sort of stock toward which I'd have gravitated without a screen-based model, I'm not going to jump out a window because its data-profile passed muster under my Buffett-inspired model.

Precision Castparts (PCP)

Like Moog discussed above, this manufacturer of castings is a company that derives most of its business from aerospace customers (65%, versus 21% from power-generation customers and the rest from the general industrial category) and requires technological prowess to succeed in its business, but is spared the sort of rapid-fire product fickleness that is antithetical to the sort of consistency required by my Buffett-inspired model. The main focus here is on strong demand for new generations of more fuel efficient commercial aircraft and more advanced fighter planes. A sustainable economic expansion, should we experience that, would further contribute to PCP's future growth.

Meanwhile, returns on equity have been in the mid-teens lately and free cash flow dwarfs capital spending needs. In January, the company completed its acquisition of Titanium Metals, and a few months earlier, PCP added to its power business by acquiring Texas Honing. But despite the attention to M&A, which is likely to be ongoing, management announced in late January that it would gradually buy back $750 million worth of common shares.

The stock trades for 19 times the estimate of current-year EPS and 16 times next year's estimate. All in all, this isn't the sexiest company around, but it seems made to order for the three key themes of my selection model: fair valuation, solid fundamentals, and reasonable consistency.

Smith & Nephew (SNN)

This company, like Varian which follows, is in the medical device business. On paper, both should be inevitable home runs. We know with 100 percent certainty that the average age of the U.S. population is aging, that older people require more in the way of medical treatment, and that we want and expect to benefit from all that is available. But there's another challenging inevitability. This stuff costs money and when it comes to paying, everybody seems adept at pointing fingers elsewhere. That makes life much more challenging for all firms in this area. The good news, so to speak, is that the cost pressures have been out there for a while now, so it says something when a company in this field can demonstrate the sort of reasonable consistency required by my model. This doesn't mean there haven't been or won't be occasional setbacks; the phrase I use is "reasonable consistency," not zero tolerance.

The company produces a wide variety of products relating to orthopedic reconstruction, trauma care (products that help repair broken bones), sports medicine (minimally-invasive joint surgery), and advanced wound management. Returns on capital from these businesses have been in the neighborhood of 20% and cash from operations, which comes after having subtracted R&D, is well above capital spending needs. Sales growth has, in recent years, felt the impact of cost-containment pressures, but SNN has three responses. One is to keep enhancing the product portfolio with M&A on the table as one way to accomplish this. Case in point: the December 2012 acquisition of Healthpoint, which adds bioactives to SNN's wound-management capabilities. Another involves efforts in the area of manufacturing efficiency, which seem to be bearing fruit as margins rose last year in the face of sluggish revenue trends. The third, and perhaps most significant, consists of efforts to serve developing-world markets where population aging is supplemented by increasing living standards which translate to increases in lifestyle-based conditions, increases in access to medical care, and more reluctance to tolerate non-treatment. The stock sells for about 14.5 times estimated current-year EPS and about 13 times next year's estimate.

Varian Medical Systems (VAR)

This producer of radiological devices for treating cancerous tumors hasn't had a down year in revenue, operating profit or EPS since before 2000, an achievement that is quite noteworthy given the cost-containment issues with which this sector has been wrestling. (I really hate saying things like that. Just my luck, I probably jinxed the company. Hopefully, that won't impact results. But at least I did mention that this has been an annual trend, not necessarily a quarterly trend. There was some order softening in the last quarter which might show up in current-quarter numbers, but management sees this as more a matter of timing than underlying demand.)

There are a lot of different products here, but the big theme is precision in targeting cancer tumors, which involves meeting a variety of challenges relating to position, shape, obstruction, and what surrounds the tumor. The unifying goal is to direct as intense as possible a beam at the tumor with minimal if any damage to surrounding tissue. Admittedly, this sounds a bit more tech oriented than many associate with Buffett. But as with others discussed here, it's not a rapid-fire fly-by-night competitors-in-competitors-out situation. VAR has been at this for quite a while and the consistency of its performance shows it's not as easy in reality as it is in theory for others to jump into the field and steal business. Returns on equity of around 30% should certainly motivate wannabe rivals (at least that's what they teach in basic economics classes). The fact that VAR's returns are holding steady in that area suggests the wannabes haven't been getting it done. This doesn't mean VAR is forever unassailable, but it seems no less so than a lot of other successful competitors Buffett has and still owns. (VAR's returns on equity are usually neck and neck with those of Coca Cola, but unlike Coke, VAR achieves them without using debt to leverage up.)

Even so, VAR isn't sitting still. Like SNN above, VAR has gone global and is looking toward developing markets, but to date, much of its international business is among more developed nations. It's also addressing other areas of X-ray technology. The stock trades for about 17 times estimated current-year EPS and 15 times next year's estimate.

No comments:

Post a Comment