Ignore Sony At Your Own Risk

I recently published an article about Sony (SNE) and how I believe it is wise to buy the stock hand over fist.

Judging from the sentiment in the comments to my article, it is pretty

clear that this is a hated trade. I believe that Sony is the trade of

the year and possibly the next few years. The reason has to do with

valuation and a key catalyst in the falling yen.

Recently, investors have taken notice that the yen is starting to fall. After bottoming out at 75, the U.S. dollar to Japanese yen conversion rate has risen to 89, an increase of almost 20% over the past year, the majority of which has come since September 2012. The Nikkei has correspondingly moved to new 52-week highs. Much has been written about Shinzo Abe's return to power in Japan and how he has pledged to strip the Bank of Japan of its independence if it doesn't support him in his goal of targeting 2% inflation. While there is still debate about his true intentions, with some analysts suggesting that he is merely posturing and won't follow through with actions, the charts of the yen and the Nikkei suggest that there is more to this than just words.

While the charts of the yen and the Nikkei are both oversold and overbought, respectively, in the short term, it is important to keep in mind that both were in decades long trends that have only just begun to reverse. As a result the move could be both very powerful and very long in duration.

What we have seen with the yen is that when a country operates with a current account surplus the currency of that country is extremely strong. A current account surplus -- the sum of the balance of trade (net revenue on exports less the payments for imports), factor income (earnings on foreign investments minus payments made to foreign investors), and cash transfers -- increases a country's net foreign assets by the corresponding amount, and a current account deficit does the reverse. Both government and private payments are included in the calculation. It is called the current account because goods and services are generally consumed in the current period.

Since 2005 Japan has had seven prime ministers, and over this time period the government has gotten little done because it has been constantly rotating through leaders. In this scenario, a government without the ability to pass through major reforms or policies is unlikely to spend money. Japan is the epitome of this: After a devastating tsunami and earthquake in 2011, Japan couldn't even pass a substantial rebuilding plan because of a lack of leadership. This has seemingly changed with Prime Minister Abe being re-elected on the platform that he would re-start the country's economic engine in part by putting through massive fiscal and monetary stimulus packages.

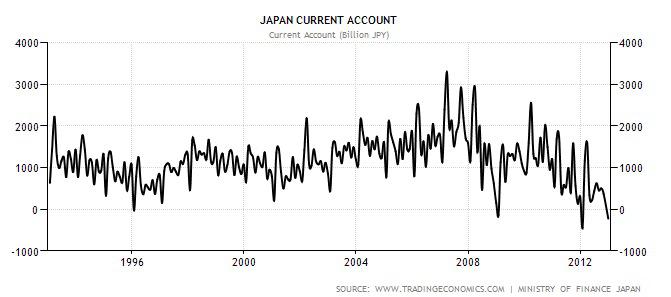

While this has been going on, Japan's current account has been deteriorating in recent years. Japan's seasonally adjusted monthly current account balance is shown below:

Click to enlarge images.

As you can see, the trend is clearly downward, and in December the deficit was the second-largest deficit over the past 20 years (the largest was earlier in 2012). Keep in mind this occurred before the proposed approximate $117 billion fiscal stimulus package had been voted on or put into place.

So what does this all mean to investors of SNE? Well, a weak currency cheapens the price of a country's exports, making them more attractive to international buyers by undercutting competitors. As a result, even the smallest move in the yen has a big impact on Japan's exporters. Consider Toyota Motors (TM), one of the country's largest exporters, which says a fluctuation of just one yen against the dollar results in a rise or fall in operating profits of $397 million over the course of a year. SNE is a huge exporter as well, having generated roughly 70% of revenues in 2011 overseas.

With the current account surplus turning into a deficit and with the government's intentions of passing through massive stimulus plans, the yen is likely to weaken significantly from here. While the yen is currently oversold and could go through a consolidation or bounce here, the likelihood of it continuing its fall is quite high.

If you combine this catalyst with its current valuation you get the recipe for a major move in the price of SNE's stock. Consider the following valuation metric: price to sales. Based on 2012 revenues, here is a list of the price to sales of some of the players in electronics and computers:

Movie Studios, for One

When looking at the valuation of SNE, which currently stands at around $11 billion, one has to look at the sum of its parts. With operations in movie studios, music, computers, cameras, cell phones, medical equipment, and many more areas, it can be difficult to assign a value to SNE as a whole. However, in looking at just one of the parts of its business, you get a sense for just how undervalued SNE is.

Consider the case of Sony/Columbia Motion Pictures. This division generated $8.1 billion in revenues in 2012, roughly one-tenth of SNE's revenues and it had a 16.6% market share, which ranked it No. 1 in the movie industry. By comparison, Lions Gate (LGF) had a 7.3% market share and has a market cap of $2.4 billion. SNE had a market share 2.27 times larger than LGF, so using simple math one could assume that SNE's motion picture business should be worth 2.27 times the market cap of LGF, or $5.5 billion. That means that the remaining 90% of SNE's business is currently only worth $5.5 billion. That is, the remaining portion of SNE's business trades at a price to sales ratio of 5.5 / 72 = 0.08.

Estimates for 2013

Right now, the consensus estimate for the year ending March 31, 2014, is for a profit of $0.92 for SNE. However, these estimates were made over the summer of 2012, prior to the most recent move in the yen. For every one-point move in the yen against the dollar, it is estimated that SNE's profits rise or fall by $30 million over the course of a year. Since the summer of 2012, the USD/JPY has risen 12 points. That alone could generate an additional $0.35 to $0.40 EPS. However, I believe the move in the yen is just getting started. After a period of near-term consolidation to work off an oversold condition, you could see a move in the USD/JPY to at least 110 (it is currently at 88) -- which could generate a total of $1.00 additional EPS for the company.

Just as importantly, the company has been going through a massive restructuring, paring down assets and focusing on its core strengths of mobile, digital imaging, gaming, and medical equipment. These cost cutting measures could add significantly to the bottom line. In June, Sony sold off its chemical operations business to a government-backed bank for $730 million and they are looking to sell their lithium ion business, estimated at $630 million and a corporate office building in Tokyo for $1 billion to $1.5 billion. These measures will help the company cut costs and raise capital to help focus on its core strengths.

Sony is projecting a modest drop in revenue for the fiscal year, ending March 2013, down to $83 billion from $85 billion compared to its earlier August forecast. The firm said its operating income projections stand at $1.6 billion as a result of new products and recent acquisitions.

Apple and Everyone Else

Over the past four months, I've written extensively about how Apple is dead money at best. I've argued that the major catalyst for its move to $700 came from the launch of the iPhone on all major carriers in the U.S. after the exclusivity contract with AT&T expired. The result of this has been what appears to be at least an intermediate top in Apple, but, more importantly, money has begun to flow to Apple's competitors that were previously left for dead: NOK is up 175% from its lows, RIMM is up 127% from its lows, and HPQ and DELL are up 50% from their lows. I believe SNE is next and is currently being ignored by investors.

Combine a shift in investor sentiment away from Apple with an extremely low valuation, a falling yen that by some estimates may have already added $0.40 in EPS, and a major cost cutting and corporate restructuring program and you have the potential for a huge winner in 2013 and 2014 in SNE. With these catalysts, there is the potential to generate $3 to $4 EPS within two years, something no one on the the Street is expecting. If this happens it is likely that the market could price the stock at 15 times earnings at some point, and you could see the stock price approach its old highs from 2007 of $50 to $60 per share.

The best part is while the recent move in the yen has sparked a major move in the Nikkei, SNE's stock price has only moved up marginally. Volume has been very heavy while the stock has traded sideways for five weeks, often a sign of a heavy accumulation.

Below is a chart of the ratio of SNE's stock price to the Nikkei. As you can see, SNE's stock is underperforming the overall Japanese market. I believe this will change shortly.

First things first, though, SNE is currently benefiting from a move in the yen, which I believe is the spark that starts the fire. I am long SNE at prices between $9.90 and $11.50. I would recommend buying it at any price below $15.00.

Recently, investors have taken notice that the yen is starting to fall. After bottoming out at 75, the U.S. dollar to Japanese yen conversion rate has risen to 89, an increase of almost 20% over the past year, the majority of which has come since September 2012. The Nikkei has correspondingly moved to new 52-week highs. Much has been written about Shinzo Abe's return to power in Japan and how he has pledged to strip the Bank of Japan of its independence if it doesn't support him in his goal of targeting 2% inflation. While there is still debate about his true intentions, with some analysts suggesting that he is merely posturing and won't follow through with actions, the charts of the yen and the Nikkei suggest that there is more to this than just words.

While the charts of the yen and the Nikkei are both oversold and overbought, respectively, in the short term, it is important to keep in mind that both were in decades long trends that have only just begun to reverse. As a result the move could be both very powerful and very long in duration.

What we have seen with the yen is that when a country operates with a current account surplus the currency of that country is extremely strong. A current account surplus -- the sum of the balance of trade (net revenue on exports less the payments for imports), factor income (earnings on foreign investments minus payments made to foreign investors), and cash transfers -- increases a country's net foreign assets by the corresponding amount, and a current account deficit does the reverse. Both government and private payments are included in the calculation. It is called the current account because goods and services are generally consumed in the current period.

Since 2005 Japan has had seven prime ministers, and over this time period the government has gotten little done because it has been constantly rotating through leaders. In this scenario, a government without the ability to pass through major reforms or policies is unlikely to spend money. Japan is the epitome of this: After a devastating tsunami and earthquake in 2011, Japan couldn't even pass a substantial rebuilding plan because of a lack of leadership. This has seemingly changed with Prime Minister Abe being re-elected on the platform that he would re-start the country's economic engine in part by putting through massive fiscal and monetary stimulus packages.

While this has been going on, Japan's current account has been deteriorating in recent years. Japan's seasonally adjusted monthly current account balance is shown below:

Click to enlarge images.

As you can see, the trend is clearly downward, and in December the deficit was the second-largest deficit over the past 20 years (the largest was earlier in 2012). Keep in mind this occurred before the proposed approximate $117 billion fiscal stimulus package had been voted on or put into place.

So what does this all mean to investors of SNE? Well, a weak currency cheapens the price of a country's exports, making them more attractive to international buyers by undercutting competitors. As a result, even the smallest move in the yen has a big impact on Japan's exporters. Consider Toyota Motors (TM), one of the country's largest exporters, which says a fluctuation of just one yen against the dollar results in a rise or fall in operating profits of $397 million over the course of a year. SNE is a huge exporter as well, having generated roughly 70% of revenues in 2011 overseas.

With the current account surplus turning into a deficit and with the government's intentions of passing through massive stimulus plans, the yen is likely to weaken significantly from here. While the yen is currently oversold and could go through a consolidation or bounce here, the likelihood of it continuing its fall is quite high.

If you combine this catalyst with its current valuation you get the recipe for a major move in the price of SNE's stock. Consider the following valuation metric: price to sales. Based on 2012 revenues, here is a list of the price to sales of some of the players in electronics and computers:

- SNE: 0.14

- Hewlett-Packard (HPQ): 0.27

- Dell (DELL): 0.4

- Nokia (NOK): 0.43

- Research In Motion (RIMM):0.68

- Samsung (SSNLF): 1.10

- Apple (AAPL): 3.08

Movie Studios, for One

When looking at the valuation of SNE, which currently stands at around $11 billion, one has to look at the sum of its parts. With operations in movie studios, music, computers, cameras, cell phones, medical equipment, and many more areas, it can be difficult to assign a value to SNE as a whole. However, in looking at just one of the parts of its business, you get a sense for just how undervalued SNE is.

Consider the case of Sony/Columbia Motion Pictures. This division generated $8.1 billion in revenues in 2012, roughly one-tenth of SNE's revenues and it had a 16.6% market share, which ranked it No. 1 in the movie industry. By comparison, Lions Gate (LGF) had a 7.3% market share and has a market cap of $2.4 billion. SNE had a market share 2.27 times larger than LGF, so using simple math one could assume that SNE's motion picture business should be worth 2.27 times the market cap of LGF, or $5.5 billion. That means that the remaining 90% of SNE's business is currently only worth $5.5 billion. That is, the remaining portion of SNE's business trades at a price to sales ratio of 5.5 / 72 = 0.08.

Estimates for 2013

Right now, the consensus estimate for the year ending March 31, 2014, is for a profit of $0.92 for SNE. However, these estimates were made over the summer of 2012, prior to the most recent move in the yen. For every one-point move in the yen against the dollar, it is estimated that SNE's profits rise or fall by $30 million over the course of a year. Since the summer of 2012, the USD/JPY has risen 12 points. That alone could generate an additional $0.35 to $0.40 EPS. However, I believe the move in the yen is just getting started. After a period of near-term consolidation to work off an oversold condition, you could see a move in the USD/JPY to at least 110 (it is currently at 88) -- which could generate a total of $1.00 additional EPS for the company.

Just as importantly, the company has been going through a massive restructuring, paring down assets and focusing on its core strengths of mobile, digital imaging, gaming, and medical equipment. These cost cutting measures could add significantly to the bottom line. In June, Sony sold off its chemical operations business to a government-backed bank for $730 million and they are looking to sell their lithium ion business, estimated at $630 million and a corporate office building in Tokyo for $1 billion to $1.5 billion. These measures will help the company cut costs and raise capital to help focus on its core strengths.

Sony is projecting a modest drop in revenue for the fiscal year, ending March 2013, down to $83 billion from $85 billion compared to its earlier August forecast. The firm said its operating income projections stand at $1.6 billion as a result of new products and recent acquisitions.

Apple and Everyone Else

Over the past four months, I've written extensively about how Apple is dead money at best. I've argued that the major catalyst for its move to $700 came from the launch of the iPhone on all major carriers in the U.S. after the exclusivity contract with AT&T expired. The result of this has been what appears to be at least an intermediate top in Apple, but, more importantly, money has begun to flow to Apple's competitors that were previously left for dead: NOK is up 175% from its lows, RIMM is up 127% from its lows, and HPQ and DELL are up 50% from their lows. I believe SNE is next and is currently being ignored by investors.

Combine a shift in investor sentiment away from Apple with an extremely low valuation, a falling yen that by some estimates may have already added $0.40 in EPS, and a major cost cutting and corporate restructuring program and you have the potential for a huge winner in 2013 and 2014 in SNE. With these catalysts, there is the potential to generate $3 to $4 EPS within two years, something no one on the the Street is expecting. If this happens it is likely that the market could price the stock at 15 times earnings at some point, and you could see the stock price approach its old highs from 2007 of $50 to $60 per share.

The best part is while the recent move in the yen has sparked a major move in the Nikkei, SNE's stock price has only moved up marginally. Volume has been very heavy while the stock has traded sideways for five weeks, often a sign of a heavy accumulation.

Below is a chart of the ratio of SNE's stock price to the Nikkei. As you can see, SNE's stock is underperforming the overall Japanese market. I believe this will change shortly.

First things first, though, SNE is currently benefiting from a move in the yen, which I believe is the spark that starts the fire. I am long SNE at prices between $9.90 and $11.50. I would recommend buying it at any price below $15.00.

No comments:

Post a Comment