http://seekingalpha.com/article/899401-good-time-to-invest-in-chinese-equities?source=email_rt_article_readmore&ifp=0

Good Time To Invest In Chinese Equities

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Equity markets tell investors more about an economy than any

data release, which can be subject to manipulation. This holds true for

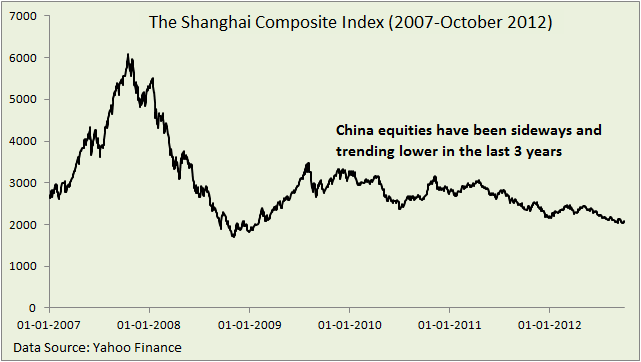

Chinese equities, which have been trending lower in the last three

years amidst talks of a sharp slowdown in China.The Lehman crisis and the subsequent credit freeze led to the Shanghai index crashing to levels of 1,706 in November 2008. Over the next one year, the index surged by 96% to 3,339 by November 2009.

(click to enlarge)

Post this period of phenomenal returns, the Shanghai index has moved sideways to lower over the next three years. Currently, the index is lower by 38% compared to November 2009 levels.

The key question for investors is: will the markets continue to trend lower for long-term, or is it a good time to buy Chinese stocks?

I am of the opinion that the Shanghai index will trend higher in the long-term and the sharp correction is a good time to gradually accumulate Chinese equities.

The stock markets generally bottom out along with the economic activity touching its lows. This was evident during the recession of 2008-09. The equity markets bottomed out globally in March 2009 and GDP growth also bottomed out during the first quarter of 2009.

I am of the opinion that the Chinese economy might be near its bottom (in terms of economic activity) and growth will stabilize at these levels before trending higher over the long-term. In line with this rationale, I believe that one can consider exposure to equities in China.

Again, one of the first reasons for believing that it might be a good time to buy China equities is the message one can derive from market movements. Over the last 24 trading sessions, the Shanghai index has been practically gone nowhere, with the index down by 0.3% during this period.

Unless there is a big negative surprise globally in terms of economic activity, I consider the current phase as a period of consolidation and bottoming out at lower levels.

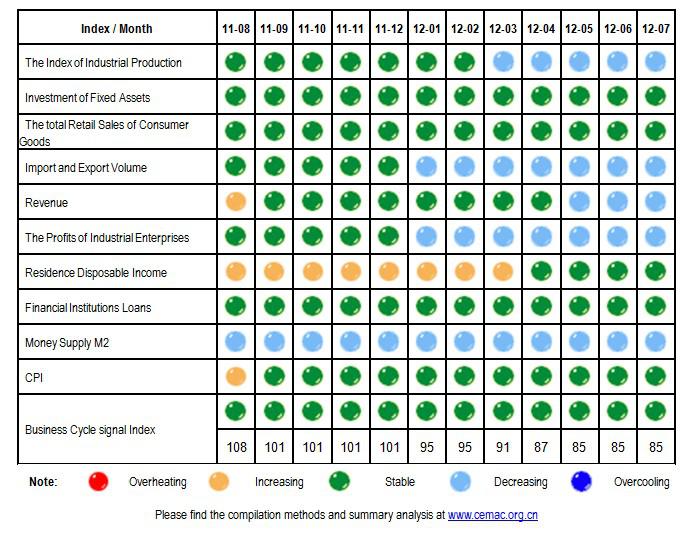

One can relate this behavior of markets with the business cycle index in China. The index has stabilized at lower levels after falling from a high of 108 in August 2011.

(click to enlarge)

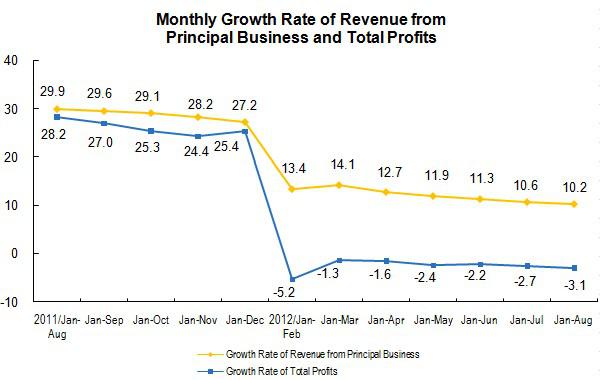

The industrial profits have also moderated in China, but are no longer in a period of freefall as witnessed during the Jan-Dec period of 2011.

(click to enlarge)

After a prolonged period of high growth, it is perfectly fine for an economy to cool down in order to clean its excesses. China is in the same phase after a long period of double digit GDP growth.

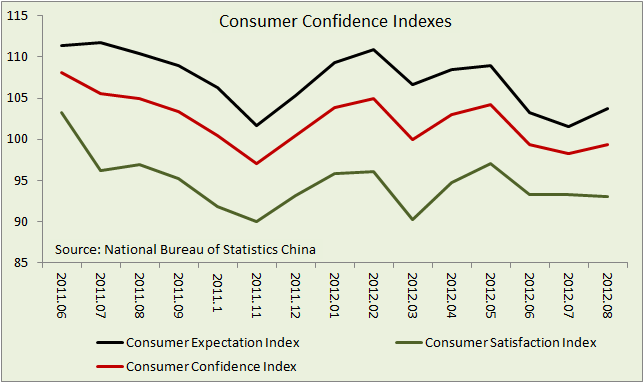

The consumer confidence index gives another reason to believe that economic activity might have bottomed out in China. The consumer expectation index ticked higher in August along with an increase in the consumer confidence index.

(click to enlarge)

I am certainly not suggesting that the Chinese economy and markets will bounce back from these levels. However, I do feel that the economy is near the bottom or has already bottomed out. The same should be the trend in equity markets.

Investors need to remember that the US had several recessions and a depression on its way to becoming the largest economy in the world. Therefore, it might not be a good idea to completely write off China just because of its manufacturing excesses.

I would personally consider exposure to the Chinese equities at these levels. Also, gradual accumulation of equities would be a good idea as the markets will not surge in a matter of a few days or months.

Investors can consider exposure to the iShares FTSE/Xinhua China 25 Index (FXI), which seeks investment results that correspond generally to the price and yield performance, before fees and expenses, of the FTSE China 25 Index. In terms of risk, the ETF has a relatively high expense ratio of 0.72%. Further, the ETF has 55.9% exposure to the financial sector in China. Having said this, markets have discounted the concerns relating to the financial sector.

The MSCI China Index Fund (MCHI) is also a good investment option with the fund seeking investment results that correspond generally to the price and yield performance, before fees and expenses, of the MSCI China Index. The fund has a relatively low expense ratio of 0.58% and has a more diversified stock and sector exposure compared to the FXI.

Among specific stocks, Baidu Inc. (BIDU) looks attractive for long-term. Baidu is the largest search engine in China and has also turned out to be a default search engine for 80% of branded Android handsets in the Chinese markets. China's internet users, currently at 538 million, are expected to pass 800 million by 2015. Being the largest player, Baidu is well positioned to take advantage of the growth in internet users. Baidu has also invested in R&D and added 5200 employees in 2011 (primarily in R&D and sales). These initiatives are expected to translate into future expansion ideas and growth for the company. Investors can therefore consider some exposure to the Google (GOOG) of China.

,

152,983 people who get Macro View daily and

62,979 people who get Global Investing daily.

No comments:

Post a Comment