On morning of 17 November, while Western investors

were sleeping, China opened the door to its investment world. On that

day China began two-way trading between the Shanghai and Hong Kong stock

exchanges. This development essentially opened the Chinese stock

market to investors around the world through Shanghai-Hong Kong Stock

Connect. They said to investors around the world, “Welcome, just bring

your money and come right in.”

Investors would be well advised to be aware of the money flowing

into the Chinese stock market, and possible ramifications of that money

movement.

Money is like water flowing across the earth, it fills in the low

spot. To foreign investors, and in particular dollar-based

institutional funds, the Chinese stock market is a “low spot” to be

filled in with money. Foreign investors will fill that “low spot” with

their money. Institutional money managers cannot ignore the most

important economy in the world, and one destined to be the largest. As

the chart at right portrays, the cumulative dollar flow into China’s

stock market is off to a good start. At present the daily limitation on

investment money inflow is 13 billion Yuan, or roughly $2.1 billion,

per day. Actual money flows have been below that limit, but it is just

the first week of the rest of time. Note especially that we only have a week of data, and the discussion that follows is about trends that will unfold over time.

In order to buy Chinese stocks one must have Renminbi to pay for

them. To a dollar-based investor that means selling dollars and buying

Renminbi. Those transactions should put downward pressure on the dollar

and upward pressure on the Renminbi. While a myriad of factors will

influence the value of the Renminbi, this money flow, which will be

massive over time, will contribute to the secular uptrend in value of

Chinese Renminbi already in place. Second chart above portrays the

cumulative money flows into Chinese stock market with dollar value of

the Renminbi. As that black line is rising, the Chinese currency is

appreciating and the dollar is depreciating. While our focus here is on

the dollar, other currencies, such as the Euro and yen for example,

will come under similar selling pressure.

As money flows out of dollars and other currencies, the value of Gold

in those currencies should rise. In the chart to the right is plotted

the cumulative flow of money into Chinese stock versus price of

US$Gold.

Another question that arises is from where will this money come.

Near all the money flowing into Chinese stocks will come from

institutional funds of all kinds, especially U.S. based speculative

funds. While we know not from where in their portfolios money for

purchases of Chinese stocks will come, one clear candidate for a money

source is the NASDAQ traded issues. Many of those stocks are over owned

in institutional portfolios. In the bottom chart is plotted again the

cumulative money flow into Chinese stocks verus the NASDAQ Composite

Index, left axis.

In reviewing this situation several possible strategies present

themselves for consideration by investors. With a money flow over

coming years into Chinese stocks that will be measured in the hundreds

of billions of dollar, buying Chinese stocks is clearly one

possibility. For a variety of reasons, this approach may not fit many

individual investors. Hong Kong exchange may be more viable and

friendly route.

Second, consideration should be given to investing in the Chinese

Renminbi as it is likely to rise in value versus your home currency.

Most desirable route is through a Renminbi denominated bank deposit.

These accounts are available through many banks around the world and on

the internet. In U.S. banks those deposits are insured. Exchange Traded

Currencies (ETCs), a form of ETF, are also available. However,

investors should probably avoid Exchange Traded Notes (ETNs).

A third alternative should be obvious from the above discussion.

Gold is a form of currency that moves opposite the value of national

currencies. Dollar and most other national currencies should depreciate

versus the Chinese Renminbi. That action should add support to the

value of Gold in those currencies. For many, this investment route may

be more comfortable than the previous two.

Finally, note that the above prognostications are the future, a time

period measured in years. They are not forecasts of what might happen

tomorrow afternoon. We prefer you become wealthier over time rather

than feed the hope for one lucky trade. Ned Schmidt, CFA www.valueviewgoldreport.com

Follow us @vvgoldreport

Oct. 6 (Bloomberg) – Bloomberg’s Stephen Engle reports on the World Bank

lowering its growth forecast for East Asia for the second time this

year, citing the slowdown in China for downgrading expectations. He

speaks to Angie Lau on “Asia Edge.” (Source: Bloomberg)

The World Bank lowered its forecasts for growth in developing East

Asia this year and next as China’s expansion moderates and policy makers

brace for tighter global monetary conditions.

The region is

forecast to grow 6.9 percent in 2014 and 2015, down from 7.1 percent

projected in April, the Washington-based lender said in its East Asia

and Pacific Economic Update released today. China will expand 7.4

percent this year and 7.2 percent next year, compared with 7.6 percent

and 7.5 percent previously forecast, the report showed.

Data

released last month showed China’s industrial-output expansion at its

weakest since the global financial crisis, while moderating investment

and retail sales growth underscore the risks of a deepening economic

slowdown led by a slumping property market. Significant uncertainties

remain that could affect the region’s growth including downside risks in

the euro area and Japan, a sharp tightening in global financial

conditions and international and regional geopolitical tensions, the

World Bank said.

“The best way for countries in the region to

deal with these risks is to address vulnerabilities caused by past

financial and fiscal policies, and complement these measures with

structural reforms to enhance export competitiveness,” Sudhir Shetty, the World Bank’s East Asia and Pacific chief economist, said in a statement.

Photographer: Brent Lewin/Bloomberg

A bicycle rickshaw driver passes by the Bell Tower in Beijing. China’s growth is... Read More

Growth in the region excluding China is expected to

accelerate to 5.3 percent in 2015 from 4.8 percent this year as a

gradual recovery in high-income economies boosts demand for its exports,

and domestic economic reforms advance in the large Southeast Asian

economies, the World Bank said.

Exports Boost

It

raised its forecast for Malaysia’s 2014 growth to 5.7 percent from 4.9

percent in April because of robust exports in the first half, it said.

The surge in shipments helped growth in the economy unexpectedly

accelerate to the fastest pace in six quarters in the three months

through June from a year earlier.

China’s growth is expected to

slow as the government implements policies to address financial

vulnerabilities and structural constraints, the World Bank said.

As

it seeks to strike a balance between containing risks and meeting

growth targets, structural reforms in sectors previously reserved for

state enterprises and services could help offset the impact of measures

to contain local government debt and curb shadow banking, the report

showed.

Protests in Hong Kong will probably slow growth there

this year but haven’t so far had a significant impact on China’s

economy, Shetty said today.

Trade Flows

The world’s second-biggest economy was the top trading partner for the 10-member Association of Southeast Asian Nation’s last year, according to data from the Asean-China Centre.

The

World Bank also cut its forecasts for Thailand’s growth this year to

1.5 percent from an earlier estimate of 3 percent. The country’s junta,

which seized power about four months ago in a coup, has said it will

stop buying farm products directly from growers as state purchases spur

overproduction, distort the market and create stockpiles.

The

country needs to pursue further fiscal reforms following the scrapping

of the rice-pledging scheme and proposals including the revision of

property income taxes warrant serious consideration by the new

government, the World Bank said.

World Outlook

The

global economy is showing signs of recovery, albeit at an uneven pace,

while significant uncertainties remain regarding the strength and

sustainability of the recovery in high-income economies and about the

timing of policy actions by central banks in these countries, the World

Bank said.

The world’s growth is forecast to be 2.6 percent growth in 2014, and an average of 3.3 percent from 2015 to 2017, it said.

“In

this uncertain global environment, there is still a window of

opportunity to enact critical, and in some cases overdue, reforms,” the

World Bank said in its report. “The short-term priority in several

countries is to address the vulnerabilities and inefficiencies that have

been created by an extended period of loose financial conditions and

fiscal stimulus.”

To contact the reporter on this story: Sharon Chen in Singapore at schen462@bloomberg.net

To contact the editors responsible for this story: Stephanie Phang at sphang@bloomberg.net Brett Miller, James Mayger

China’s

long-term growth outlook is solid, but there will be rocky times along

the way. Figuring out when those rocky times will hit is difficult.

Businesses involved in China for the long term can be confident of

economic growth, but the company that needs strong sales in one

particular year is much less certain.

In this article we’ll look at the drivers of China’s long-term

growth, then address the short-term challenges. I’m not a China expert,

but the country is important to some of my clients so I take an

outsider’s view of the statistics and stories coming from the country.

First, though, let’s address the question of whether we spend too

much time talking about China. China is the second largest economy in

the world and the United States’ second-largest export destination. Many

commodity-based economies have risen in recent years with China’s

growth. Moreover, China’s opportunities and challenges are similar to

what other emerging countries are facing, so it’s a bellwether for a

larger group of countries.

China’s long-term growth story is fairly simple. In the late 1970s,

Deng Xiaoping enacted reforms to allow farmers to cultivate family plots

rather than communal farms. He tolerated small entrepreneurs. A

migration from poor rural areas to cities with opportunities was ignored

though it was illegal. These reforms substantially raised the

productivity of poor people in the country. Foreign investment followed,

further increasing productivity. Trade with other countries increased,

again tolerated by the government. In short, economic reforms allowed

poor people to become more productive, and they earned rising incomes.

This story won’t go on forever, but there’s substantial room for further gains. China ranks 93rd

in the world on GDP per capita, indicating substantial room for

improvement. China’s per capita output would have to grow by 32 percent

just to match the current world average. It would have to more than

triple to equal the European average. There’s no reason China won’t

eventually get close to the output level of the developed world. That

will drive above-average growth rates for many years. The Economist has noted a decline in the number of Chinese who

are of working age, caused by the one child policy. The policy began in

1979, so the first wave of only-children is now 39 years old, about

halfway through their working years. The Economist calls the

phenomenon “peak toil,” but it is less relevant to China than to a

developed country such as Japan. In China, increased productivity of

existing workers is the huge force, while growth of the total labor

force is a relatively small factor.

Although the long-term outlook is positive, the country’s transitions

create stumbling blocks. Environmental concerns are one major issue. By

some reports, some domestic coal and iron ore is not being used because

it’s too dirty; instead, steel and coal are imported. Factories are

expected to clean themselves up, with short-term adjustment costs.

The mix between exports and domestic consumption is another

short-term issue. Early on, the great surge of output was for

international markets. Rising incomes have caused a growing consumption

economy, and the transition is not totally smooth.

With rising incomes have come rising real estate prices, leading to a

housing boom. Some analysts anticipate a hard landing from the boom,

but so far it’s been fairly soft. However, this is another transition

that presents an obstacle to a smooth path for the Chinese economy.

Rising wages have also caused a loss of some of the substantial cost

advantage that China has had, with additional loss from the rising

foreign exchange rate. Some American companies are “re-shoring” their

operations. Costs are still lower in China, especially for

labor-intensive work, but lower costs don’t always cover higher

transportation costs, quality monitoring costs and the economic loss

from a longer supply chain.

Chinese consumers are increasingly concerned about the quality of the

products they buy, especially after the 2008 contaminated milk scandal.

This concern is strongest in food products, but also extends across all

locally made products, including apparel and kitchen gadgets. Local

companies producing for the local market, however, are used to cutting

corners. Chinese companies that produce high quality exports for the

likes of Apple are not producing much for their own market. Eventually,

companies will match their production to the quality that consumers are

willing to buy, but the transition is likely to be ragged.

China’s political leaders understand, or at least give lip service,

to the need for further structural reforms, especially in credit

allocation. The first default on a bond issue in the country is actually

good news in this regard, indicating that problems will not always be

swept under the rug. Political leaders have also begun an

anti-corruption campaign, which sounds like foxes guarding the chicken

coops. Altogether too much cronyism occurs in the nation’s

political-economic decisions.

An economy is not really about aggregates such as gross domestic

product or industrial production. Actual goods and services are produced

and sold to particular consumers, businesses and government

departments. A smoothly-functioning economy gets the right goods

produced and sold at the right prices. A good economy also adjusts the

composition of output to reflect changes in tastes, technology and

materials costs. However, the more changes that need to be made, the

harder it is to get all of the production and consumption decisions

right. China has many changes to make. Their economic system still has

too much cronyism and protection of state enterprises, which slow down

adjustments.

China is likely to have a pronounced slump in the next few years—but a

temporary slump. Continued smooth growth is simply too much to hope for

in a somewhat-clumsy economy subject to numerous major transitions.

When this slump occurs is impossible to predict. As in the United

States, some analysts are always bearish and some always bullish. It’s

unlikely that anyone will switch from bull to bear at exactly the right

time.

The IMF predicts very gradual deceleration in the coming years,

and that’s a fine forecast—if nothing goes wrong. My advice is to plan

for long-term growth, but also do contingency planning for a sharp,

short-lived recession sometime in the next few years. Just when it will

occur, however, I cannot say.

[Updated 7/21/2014 to correct the name of Deng Xiaoping.]

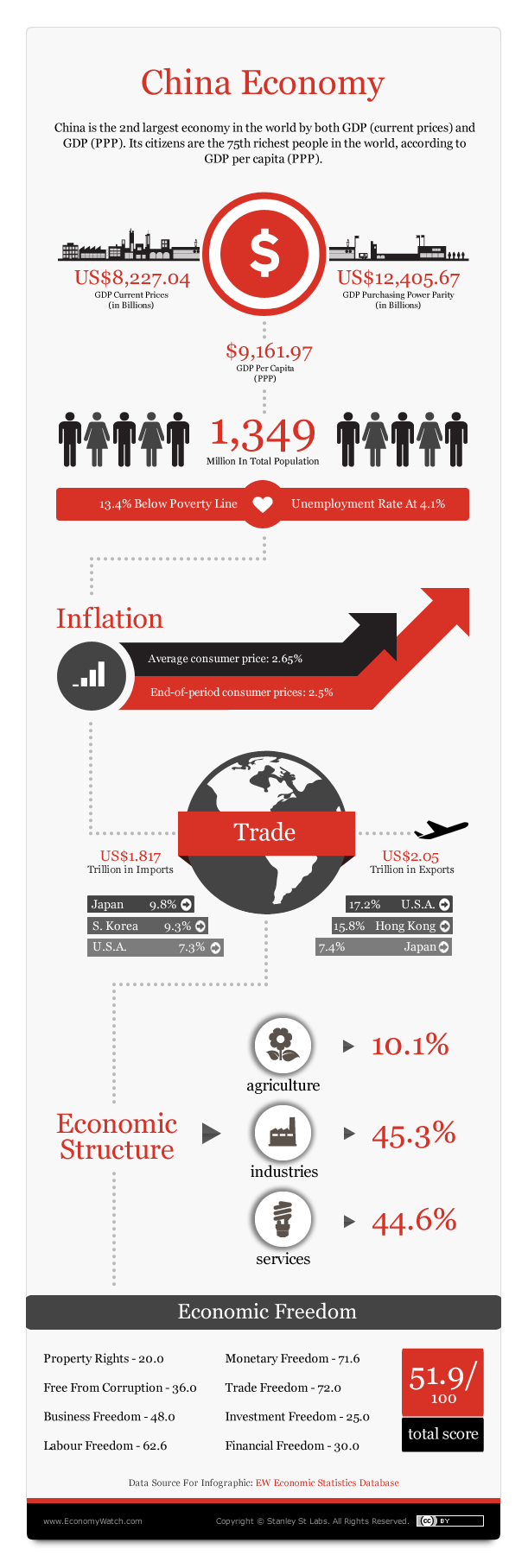

China

is the 2nd largest economy in the world according to both GDP (current

prices, US dollars) and GDP (PPP). In 2012, China’s GDP (current prices,

US dollars) was US$8.227 trillion and its GDP (PPP) was US$12.405

trillion.

In 2012, China was the 18th fastest growing economy in the world,

with a real GDP growth rate (constant prices, national currency) of 7.8

percent. Although the figure is its slowest growth since 1999, it is

also representative of a maturing economy as it gradually transition

from a developing to developed nation.

Since 1949, the Chinese government has been responsible for planning

and managing the national economy. But it was only in 1978 – when Deng

Xiaoping introduced capitalist market principles –that the Chinese

economy began to show massive growth, averaging 10 percent GDP growth

over the last 30 years. During that period the size of the Chinese

economy grew by roughly 48 times, from $168.367 billion (current prices,

US dollars) in 1981 to $8.227 trillion.

From 2003 to 2010, the Chinese economy experienced near-uninterrupted

double-digit growth – with the exception of 2008 and 2009, during the

global economic downturn. Nevertheless, the Chinese economy still

managed to post respectable growth figures during that period – 9.635

percent and 9.214 percent respectively.

China Economic Forecast

In 2013, its GDP (PPP) is expected to reach $13.623 trillion – or a

9.81 percent increase. Comparatively, China’s GDP (PPP) grew by 9.73

percent from 2011 to 2012. Forecasts for the next five years predict the

nation’s GDP (PPP) will grow by an average of 13.24 percent per annum,

reaching $22.641 trillion in 2018. Nonetheless, while its GDP (PPP) is set to overtake that of the

US’s, China’s nominal GDP (current prices, US dollars) will still be

below that of its rival in 2018. The US’s GDP (current prices) is

forecasted to hit $21.101 trillion in five years, significantly higher

than China’s $14.911 trillion. Going by current growth rates, it will

take another 30-40 years for China to become the world’s largest economy

in both GDP (PPP) and GDP (current prices).

Since initiating market reforms in 1978, China has shifted from a

centrally planned to a market based economy. More than 600 million

citizens have been lifted out of poverty as a result, but over 170

million people still live below the $1.25-a-day international poverty

line. In 2012, China’s GDP (PPP) per capita was $12,405.67. This is 37

times higher than what it was just 30 years ago. By 2018, China’s GDP

(PPP) per capita will climb from the 90th to 75th highest in the world –

at $16,231.50. This however will still be below the forecasted world

average of $18,867.17. Find out more about the Chinese Economic Forecast on the Economy Watch Economic Statistics database.

China Economic Profile

China Economic Structure

China has one of the most diverse spread of industrial production in

the world, fitting for a country that is called 'The World’s Factory'.

Since 1978, the nation has gradually reduced its reliance on state-owned

enterprises (SOEs) – though they still account for 46 percent of

China’s industrial output, down from 77.6 percent 35 years ago

Nonetheless, the government has in recent years renewed its drive to

support state-owned enterprises in sectors it considers important to

national economic security – particularly natural resources, banking and

telecommunications. In a major push to boost the state sector in 2003,

Beijing set up the State-owned Assets Supervision and Administration

Commission as a watchdog to expand and strengthen large industrial state

enterprises.

Consequently SOEs, combined assets rose to 28 trillion yuan ($4.56)

2011 from 7.13 trillion yuan in 2002. Revenues have also soared from

3.36 trillion yuan to 20.2 trillion yuan.

Critics argued that the SOEs are stifling innovation and restricting opportunities for private companies. Though

fewer in number than before, as a result of massive state

consolidation, today’s SOEs are far more powerful. As of 2012, large

state-owned enterprises produced over 50 percent of China’s goods and

services and employed over half of the nation’s labour force. 65 of the

Chinese SOEs also made it into 2012 Fortune Global 500 list, including

State Grid Corporation of China, which operates the country's power

grid, and oil companies China National Petroleum Corporation and

Sinopec.

The Chinese economy can also be understood as a decentralised

collection of several regional economies, with large imbalances between

the rural and urban population.

The three wealthiest and most important economic regions are all on

the east coast: the Pearl River Delta close to Hong Kong, The Yangtze

River Delta surrounding Shanghai and the Bohai Bay region near Beijing.

It is the rapid development of these areas that is expected to have the

most significant effect on the Asian regional economy as a whole, and

Chinese government policy is designed to remove the obstacles to

accelerated growth in these wealthier regions.

Over the past two decades however, China has embarked on an ambitious

program of expressway network expansion. By facilitating market

integration, this program aims both to promote efficiency at the

national level and to contribute to the catch-up of lagging inland

regions with prosperous Eastern ones.

The consequence of the program saw China’s two major financial

centres, Beijing and Shanghai, experience the lowest growth in 2012 –

7.7 percent and 7.5 percent respectively – compared to growth rates of

over 13 percent for Tianjin, Chongqing, Guizhou, Yunnan in the more

impoverished interior. Find out more about China Economic Structure on EconomyWatch.com

China Exports, Imports and Trade

China is the world’s second largest trading nation behind the US –

leading the world in exports and coming in second for imports. From

2009-2011 its trade to GDP ratio was 53.1 percent, while its trade per

capita was $2,413.

Since its accession into the WTO in 2001, China‘s share in global

trade has doubled – accounting for 10.38 percent of the world’s

merchandise trade exports and 9.43 percent of merchandise trade imports. For many countries around the world, China is rapidly becoming

their most important bilateral trade partner. In 2011, they were the

largest exporting/importing partner for 32 and 34 countries

respectively.

However, there have been concerns over large trade imbalances between

China and the rest of the world. The US in particular has the largest

trade deficit in the world with China at $315 billion, more than three

times what it was a decade ago.

There have also been a growing number of trade disputes brought

against, mainly for dumping, unfair subsidies by the Chinese government,

intellectual property and the valuation of the yuan. Nonetheless its

WTO entry ensures that the country will remain a key figure in

international trade.

Domestically, the Chinese government has been keen to reduce the

economy’s reliance on exports and focus on internal consumption. In

March 2013, China’s new leadership announced that they would move to

recalibrate the economy, acknowledging that there is a “growing conflict

between downward pressure on economic growth and excess production

capacity.” Find out more about China Exports, Imports & Trade on EconomyWatch.com

China Industry Sectors

The most dominant sector of China’s economy remains its manufacturing

and industries. Despite seeing a 3.3 percentage point drop in its

composition of the nation’s GDP, industries still accounted for 45.3

percent of China’s GDP in 2012 – cementing China’s position as the world

leader in gross value of industrial output. Nevertheless, despite the dominance of Industries in the

composition of China’s GDP, Services is catching up quickly – and may

overtake Industries by the end of the year. In 2012, Services accounted

for 44.6 percent of China’s GDP, just 0.7 percentage points behind

Industries. Comparatively just three years ago, that gap was 8.1

percentage points wide.

Finally, Agriculture accounted for 10.1 percent of China’s GDP in

2012. The economic reforms introduced in 1978 saw China de-collectivize

agriculture, yielding tremendous gains in production as a result.

Today, China is the world's largest producer of agricultural products

- ranking first in the world for rice, wheat, potatoes, sorghum,

peanuts, tea, millet, barley, cotton, oilseed, pork, and fish. About 300

million Chinese are employed in the agriculture sector – making up 34.8

percent of the labour force. Find out more about China Industry Sectors on EconomyWatch.com

China's economy is growing into multiple new sectors. For example,

the eCommerce sectors has been growing, both with large sites such as Alibaba, and with multiple small retailers, such as this site, offering clothes shopping online.

The mix between exports and domestic consumption is another

short-term issue. Early on, the great surge of output was for

international markets. Rising incomes have caused a growing consumption

economy, and the transition is not totally smooth.

The mix between exports and domestic consumption is another

short-term issue. Early on, the great surge of output was for

international markets. Rising incomes have caused a growing consumption

economy, and the transition is not totally smooth.